The layout of the township economy: the surprising spatial distribution of informal township enterprises

Introduction

The revitalisation of township economies and of the informal sector appear to have gained traction in some policy circles at national, provincial and metropolitan levels in South Africa.[1] While much research has been done on the informal sector over the past decades, there are still many knowledge gaps relating to the ways in which to support the informal sector and township economies in order to stimulate employment and income growth.

Little is known about the layout and spatial context of local township economies and the factors that make certain businesses more active (and successful) in certain locations in the township than in others. This article reports on research that seeks to address that knowledge gap (Charman & Petersen 2014). It quantifies as well as qualifies the diversity, frequency and vibrancy of the informal economy in the townships through a comprehensive investigation of five townships around Cape Town. Some surprising patterns are revealed.

Using a small-area census: how and why

In our understanding of the informal sector and township economy, there is a gap between knowledge derived from national surveys (such as the quarterly labour force survey, or QLFS) and from small-scale, sector-specific case studies. The small-area research approach seeks to address this knowledge gap. It can generate new insights into the informal economy in townships and especially the spatial dynamics of the distribution and functioning of micro-enterprises in urban townships.

The research involved a so-called small-area census in each of five residential townships around Cape Town (see Charman et al. 2015). The investigation, done between November 2010 and February 2013, aimed to identify and record all economic activities and micro-enterprises, even those that were not necessarily recognisable businesses as such but which were run for economic survival or to supplement household income. The sites surveyed – Brown’s Farm, Delft South, Imizamo Yethu, Sweet Home Farm and Vrygrond – comprise a range of formal and informal residential settings.

The research used both quantitative and qualitative tools. For the small-area census, a team of researchers traversed these areas on bicycles and recorded all identified business activity (regardless of size or nature) within an area of 6 000–10 000 households. In a second phase, more than 1 500 interviews were conducted with up to 90% of the businesses in key sectors, such as the liquor trade and grocery/spaza shops.[2] Mapping GPS locations also allowed us to examine each settlement’s design, street grid and proximity to business centres and transport nodes. Qualitative data and interviews provided insights into the broader environment and the constraints under which these enterprises operate.[3]

The scope and scale of micro-enterprise activity

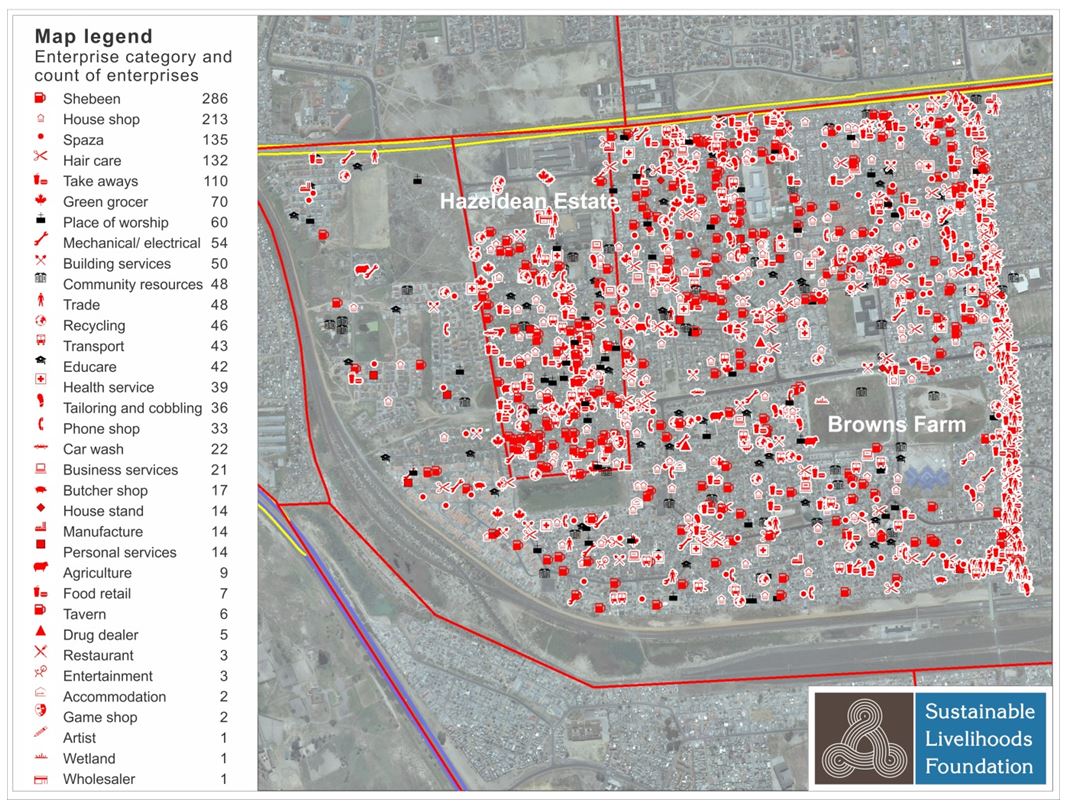

Across the five sites the researchers found 3 985 individual micro-enterprises that are engaged in 4 273 micro-enterprise activities. These were categorised as 35 types, which are illustrated by the legend of the map of micro-enterprises at Brown’s Farm (see Plate 1, which also shows the spatial distribution of the enterprises).

Plate 1: Distribution of micro-enterprises in Brown’s Farm

There are broadly similar patterns in the occurrence of micro-enterprises in the five sites. Most township businesses respond to the local population’s needs for food (groceries and takeaways), liquor, household necessities, airtime, hair-care services and entertainment. A much smaller proportion of businesses responds to needs relating to home improvement, furniture or other types of goods and services.

In terms of absolute numbers, retail sales of liquor and grocery shops are the most common micro-enterprise sectors in the sites surveyed – respectively 20% and 15% of businesses are in these two categories. Together, the top three categories (liquor, spaza shops[4] and house shops) make up 46% of the identified enterprises. Hair care, takeaway food, religious services, street traders, mechanical repair services, green grocers and recycling follow in that order; other notable sectors are educare and healthcare services.

For the five sites together there are on average 32 micro-enterprises per 1 000 people (and approximately 10 per 100 households). The number of businesses per 1 000 people varies somewhat between the sites. The highest number of informal micro-businesses (51 per 1 000 people) was recorded in Sweet Home Farm, an informal settlement on the Cape Flats. It is followed, at 39 businesses per 1 000 people, by Imizamo Yethu (a settlement in Hout Bay which has both an informal and a formal section). The lowest rate, at 21 per 1 000 people, was found in Delft South – a mainly residential township with formal housing on the Cape Flats.

Overall, the results indicate higher rates of informal business activities in informal settlements than in more formally established settlements (such as Delft South and Vrygrond). The reasons are not related only to the degree of (in)formality of a settlement, but include socio-cultural influences and factors linked to the settlement’s location (see Charman & Petersen 2014).[5]

The main components of the average of 32 businesses per 1 000 people are: liquor (8.2 per 1 000 people), spaza shops (5.3), house shops (3.6), take-away food (2.1) – with hair care (2.0) as a surprisingly large sector. The occurrence of these types of businesses varies between sites, reflecting the particular context of both the site and the settlement. For example:

• Liquor retail businesses are more frequent per 1 000 people in predominantly informal settlements. Imizamo Yethu and Sweet Home Farm have approximately 14 and 12 liquor shops per 1 000 people respectively – their most dominant business type by far. At the other extreme, Delft South (with mostly formal housing) has fewer than three liquor shops per 1 000 people – there are fewer liquor shops than spaza shops and house shops.[6]

• On the other hand, there is little variation in spaza shops, with similar numbers (approximately 4 to 5 per 1 000 people) in most of the sites.

• There is considerable diversity across the five sites in the incidence of businesses such as green grocers, health services, business services, recycling businesses and mechanical repair services. This variation is due to various factors, including the dynamics in a specific settlement, the proximity to formal businesses in commercial or industrial areas, the local infrastructure and demographic factors such as the cultural demand for traditional medicines.On the other hand, there is little variation in spaza shops, with similar numbers (approximately 4 to 5 per 1 000 people) in most of the sites.

• There are far fewer businesses in areas where there are fewer houses and/or where the neighbourhood becomes more characteristically middle class (detached houses, higher rates of vehicle ownership and so forth).

Spatial analysis: suburb, township, ‘high street’ & residential areas

Suburb versus township

In typical ‘first-world’ cities and towns, one observes a fairly clear demarcation of residential areas, core commercial areas (city centre or mega-mall areas) and shops and shopping centres along major roads (‘high streets’) that feed into residential areas. (Industrial areas constitute another category.)

As Plate 1 illustrates, in the township economy there is likely to be much less spatial differentiation: informal enterprises are found throughout the township, notably including residential areas – and not just in commercial areas or along the ‘high street’. Typically there is a mild degree of spatial differentiation that is seen in the form of a clustering of enterprises around one or more ‘high streets’ (while there rarely is a ‘township centre’ as such). The prevalence of enterprises in residential areas is one of the most pertinent characteristics found in the ‘layout’ of the townships; it has many implications for policies intended to promote township economic development (see below).

In essence, a conventional city suburb usually reflects the fact that the area has been planned as one in which there are motorised transport, roads and utilities – on a scale designed to match and accommodate a particular population density. In contrast, the township environment has developed more spontaneously and on a much smaller, walking-distance scale – rather than being a reflection of town-planning principles or urban infrastructure considerations. In a township community, high population densities are served by enterprises that locate in the immediate proximity.

Township ‘high streets’ versus residential areas

Amidst the overall low spatial differentiation, there is a second layer of differentiation. This regards the types of enterprises found mostly in residential areas versus in the ‘high street’. The high streets are identified as arterial roads and streets in which much activity takes place, but excluding local residential streets.[7] High streets sustain different kinds of business in scale and scope compared to the overall distribution.

Though there are no strict patterns, the following is apparent in the five sites surveyed. (These patterns appear to be influenced by factors such as the site’s age and history, formal-informal mix, cultural and immigrant mix, and so forth – in addition to micro-locational market and economic factors.)

On average, (only) 23% of the total number of businesses are found on the high street. In the five sites surveyed, more than three-quarters of enterprises were located outside the high-street areas in other streets and in broadly residential areas – as demonstrated in the picture of Brown’s Farm (Plate 1). Simply put: the township enterprise economy – i.e. the township’s informal business sector – is everywhere in the township.

Of those businesses on the high street, the most frequently-occurring ones are: hair care services (15%), grocery retail (spaza) (12%), take-away food (9%), liquor (8%), house shops (7%) and green grocers (6%). On average, 54% of the hair care businesses are located on the high street and 46% of the green grocers – but only 18% of the grocery/spaza shops. In mostly informal areas such as Imizamo Yethu and Sweet Home Farm, where few formal streets extend through the township, a higher proportion (29%) of grocery/spaza shops are found on the high streets. [8]

Perhaps surprisingly, the majority of liquor stores, spaza shops and house shops are located away from high streets. This means that the most numerous types of enterprises actually are not situated in what one would expect to be the prime business area, i.e. the ‘high street’ with all its pedestrian (and/or motor) traffic. They are in the residential areas.

Liquor retailers and spaza shops are situated largely in residential areas in response to highly localised demand, with people preferring to consume liquor and purchase groceries in their own neighbourhoods. These neighbourhood shops tend to be roughly equidistant from each other, with each shop serving a small local market without much competition from similar shops close by. There appears to be limited price competition amongst spaza shops, for example, because convenience appears to outweigh the potential savings from shopping outside the close local area/neighbourhood.[9]

The localised-demand dynamic implies that liquor stores, spaza shops and house shops are not much influenced or restricted by the area’s infrastructure or pedestrian and traffic volumes. Hence, their preferred location is frequently in residential areas.[10]

The residential enterprises in particular reflect the consumers’ need for day-to-day products – a requirement which is both practical (e.g. because of the lack of motor vehicles) and economic (due to limited financial resources). The township economy of micro-enterprises has evolved in a relative absence of state or planning considerations.

Conclusion

The great number of enterprises in residential areas is one of the most significant characteristics of the informal economy in townships and reflects the way in which it has emerged and grown organically to meet local demand. This has many implications for policies that intend to promote economic development in the townships. In particular, efforts to ‘streamline’ the township economy into resembling that of a ‘first-world’ town – by driving enterprises from residential areas – are likely to be counterproductive and will greatly disrupt the lives of township consumers as well as owners and employees of informal enterprises. Rather, policy efforts to support informal enterprises in townships should fully take into account the way that various demand, supply and other factors determine the locational choices of entrepreneurs.

References

Charman A & Petersen L. 2014. Informal micro-enterprises in a township context: A spatial analysis of business dynamics in five Cape Town localities. REDI3x3 working paper 5.

Charman A, Petersen L, Piper L, Liedeman R & Legg T. 2015. Small area census approach to measure the township informal economy in South Africa. Journal of Mixed Methods Research, February.

[1] At the national government level, the new Ministry of Small Business has inherited, from the Department of Trade and Industry, the brand-new National Informal Business Development Strategy (NIBUS). At the provincial government level, Gauteng and the Western Cape have recently launched new policy initiatives, while the Cape Town, Johannesburg, Durban and Bloemfontein metropolitan areas have active (if still small) initiatives in place to stimulate informal enterprises.

[2] For more detail on the research methodology, see Charman et al. (2015). A short video of the process can be viewed at: https://www.youtube.com/watch?v=WOszO8T23h8

[3] The business interview focused on the owners’ characteristics; the history, start-up and growth of the enterprise; indicators of the enterprise’s longevity, size and scale; as well as the challenges and constraints (including the effect of crime and policing).

[4] A spaza shop was defined on the basis of operations and features. To qualify as a spaza shop, it had to be open five days or more per week, have a dedicated refrigerator, signage, and sell at least eight of ten core products, including bread, milk, cigarettes, cool drinks, maize meal and rice. Should the enterprise not meet these criteria, it was considered a much smaller ‘house shop’.

[5] These figures may also suggest that there are proportionally more micro-enterprises relative to the population in predominantly black African townships in which there are large informal settlements than in mixed race and/or predominately coloured townships with more formal settlements (e.g. Delft South).

[6] The lower number of liquor businesses in the Delft area may also be attributed to there being more licenced (i.e. formalised) liquor sellers as well as, possibly, anti-alcohol sentiments of Muslim residents.

[7] High street trade is influenced significantly by peaks and troughs as the day progresses, being busiest in the morning and evening as workers make their way to and from work and generally more quiet during the day.

[8] Service businesses, such as appliance repair shops and building services are also very reliant on the high street for business, as are restaurants and car washes, with respectively 73% and 58% of them being on the high street on average.

[9] In the case of liquor traders, there are even smaller niches, within these local markets, where several businesses can operate within close proximity, each catering for a different client base in terms of age, gender or nationality an thus securing a sub-segment of the local market. This phenomenon is apparent in the high number of liquor retailers in the informal settlements.

[10] Typically, in residential areas, the rest of the business mix – apart from liquor traders and grocery/spaza shops – largely comprises enterprises that are engaged in the following: take-away foods; house shops selling chips, sweets, cigarettes, ice-cream, cool drinks and meat; game shops, and businesses involved in recycling.

Download article

Post a commentary

This comment facility is intended for considered commentaries to stimulate substantive debate. Comments may be screened by an editor before they appear online. To comment one must be registered and logged in.

This comment facility is intended for considered commentaries to stimulate substantive debate. Comments may be screened by an editor before they appear online. Please view "Submitting a commentary" for more information.