Predicting the impact of a national minimum wage: are the general equilibrium models up to the task?

Introduction

As part of an ongoing debate over the possible implementation of a national minimum wage (NMW) in South Africa, various economic modelling exercises have been undertaken. Two of these, by National Treasury (MacLeod 2015) and the Development Policy Research Unit (DPRU 2016) estimate the potential consequences of a NMW using neoclassical ‘computable general equilibrium’ (CGE) models. These seem to have been influential in shaping government’s position.

We demonstrate here that such neoclassical CGE models, due to the design of the model and the assumptions made, necessarily produce a prediction that rising wages will lead to unemployment and economic deterioration. Given this, we argue that the results of these models cannot to good effect be used to guide policy making with regard to minimum wages (for a fuller exposition see Storm & Isaacs 2016).

Unfortunately, the National Treasury and DPRU provide very limited information on their modelling assumptions, while the DPRU shows results for just a few variables. This is problematic for a critical debate. Accordingly, we also draw on likely forerunners of their models,[1] as well as well as on other contributions (DPRU 2008; Pauw 2009; Pauw & Leibbrandt 2012).

What is a CGE model?

CGE models are one kind of macroeconomic model, comprising a large number of mathematical equations that aim to represent the complex ways in which an economy works. In an attempt to mimic how changes in one part of the economy are transmitted to other parts of the economy, these equations link different sectors (like agriculture, manufacturing and services) to each other through detailed supply and demand inter-relationships. For each sector, supply is influenced by relative prices, the size of the market and technology, whereas demand depends on incomes (effective purchasing power), relative prices and consumer preferences.

The equations of the model will determine which variables are assumed to affect one another. In addition, the direction of causality (i.e. which variable determines the other) must be assumed. In neoclassical CGE models, these equations and assumptions are based on neoclassical economic theory: it is assumed that the economy behaves as neoclassical theory predicts, rather than consciously relating the model to empirical reality (which may not conform to the neoclassical assumptions). Typically these assumptions include the idea that markets are perfectly competitive and that all markets clear (i.e. they are able to reach a state of ‘general equilibrium’). Importantly, rapidly adjusting prices play the dominant role in attaining equilibrium. The magnitude of the response coefficient that is attached to each variable determines the extent to which a change in one variable affects another. In other types of models these are estimated using past statistical data, but in the case of CGE models they are, in the main, assumed (decided) by the model builder or ‘calibrated’ on the basis of an arbitrarily chosen benchmark year.

To simulate or test the likely effects of a policy step, a simulation (or scenario) exercise is performed. At the start of the simulation, one variable is ‘shocked’ (altered) which sets off a chain reaction throughout the model. The simulation is complete when the model of the economy, as constituted by the numerous mathematical equations, reaches equilibrium again. The simulated effect of the shock on other variables can then be read off the new values of these variables.

A key question is how well the economic behaviour in this simulated economy approximates behaviour in the real-world (South African) economy.

Predictions from the South African CGE models

The modelling exercises analysed here comprise different scenarios. They involve trying out different levels for the NMW and generating corresponding predictions for how the economy will likely react (with 2015 as reference year). The predictions by the DPRU and the National Treasury uniformly indicate a deterioration in the South Africa economy, even at extremely low levels of the national minimum wage.

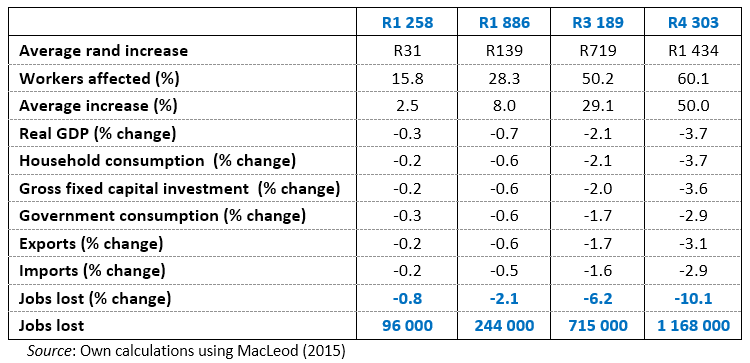

Table 1 shows the predicted outcomes from the National Treasury for different possible levels of a NMW.[2] Column 1 shows a prediction that, for the lowest NMW of R1 258 per month, only 16% of workers would benefit from receiving higher wages and the average increase per worker would be only R31, or 2.5%.[3] The total wage bill of the country would increase by a mere R52 million. The Treasury model predicts that, as a result of this (low) minimum wage, 96 000 jobs would be shed and all indicators of the state of the economy would deteriorate.

Progressively higher levels of the minimum wage are predicted to result in greater economic harm. When the NMW is set at R4 303, real GDP, household consumption, gross fixed capital investment, government investment, imports and exports all fall by between approximately 3% and 4% – and job losses are predicted to be approximately 1.2 million.

Table 1. National Treasury predictions

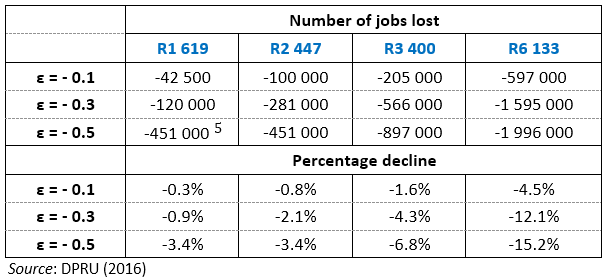

The DPRU results in table 2 show a similar progression: the higher the national minimum wage, the higher the predicted job losses. Note that the DPRU predictions are presented for different values of ε, which is the assumed ‘wage-employment elasticity’. This is a measure of how strongly employers react to wage-cost increases.[4] Thus, the predictions in the three DPRU scenarios vary hugely – which does not help much in understanding the likely impact.

Table 2. DPRU predictions

Given the different NMW levels used by the DPRU and the National Treasury, a direct comparison is difficult. However, the job losses (897 000) predicted by the DPRU for a NMW of R3 400, when assuming a -0.5 elasticity, are relatively close to those of the National Treasury’s R3 189 level (715 000 jobs shed). This is not surprising, given that the National Treasury model assumes a -0.5 elasticity.

Note that the lowest NMWs modelled by the DPRU and the National Treasury are well below the lowest current sectoral minimum of R1 994 (for domestic workers in non-major urban centres). Predicting that even such a very low NMW would have such considerable negative consequences casts significant doubt on the realism and credibility of these predictions. Other South African CGE models similarly predict up to half a million jobs lost.[5]

Such dire (and off-the-mark) outcomes match the results of CGE modelling exercises elsewhere. In Germany, anywhere between 360 000 and 2 million job losses were predicted (Schmöller 2014), while actual data show an increase in employment after the implementation of a NMW in January 2015 (Amlinger et al. 2016, for UK see Minford 1998).

As noted by the DPRU itself, international econometric studies that have analysed the impact of minimum wages after the fact (rather than predicting the outcome) clearly indicate that: ‘overall…moderate increases in minimum wages result in little or no decrease in employment’ (2016, p. 12). Similarly, for South Africa no negative employment impact was found in five out of six sectors studied (Bhorat & Mayet 2013, Stanwix 2013).

The substantial negative impact, even of low levels of the minimum wage, suggests that CGE models are intrinsically predisposed towards generating a prediction of a high level of job destruction and economic deterioration as a result of rising wages. We turn to this issue now.

Issue I: Employers’ responses to wage increases

It is logical to assume that firms within the economy should adjust to an increase in input costs – in this case from an increase in wages. In neoclassical CGE models, because of the dominant role of (relative) prices in the model, such responses are heavily restricted: firms ‘essentially have two options available to them…they can either reduce the employment of minimum wage workers by substituting them for other factors of production, or they can absorb the cost increases and pass these on to consumers in the form of higher price. […] In practice firms will opt for a combination of the two cost mitigation options’ (Pauw 2009:141–2).

However, the empirical literature shows that these are not the only adjustments available. Real-world firms make many other, important adjustments in the face of higher wages. The most common are: productivity increases where workers are assisted to produce more; so-called efficiency wages in which workers are paid more to get better performance and reduce job turnover; redistribution from high earners to low earners within firms; and a reduction in profit margins. Less often small changes are made to the number of hours worked or non-wage benefits (see, for example, Schmitt 2013; Low Pay Commission 2015). These are not captured properly, if at all, in the CGE models.[6] Moreover, the two adjustments central to the models’ response to higher wages – rising prices and falling employment – are precisely those that in real world studies have been shown not to occur, or to occur only very modestly.[7] The fact that neo-classical CGE models rely on these already indicates they may not be appropriate for modelling minimum wages.

Issue II: The multi-faceted impact of wage increases on incomes

Intuitively, it seems rational for profit-maximising firms to reduce the use of a relatively more expensive input (e.g. labour) and raise the usage of the relatively cheaper input (e.g. machines). This substitution effect is reflected in typical CGE models by rising unemployment when wages are raised, with the extent of the employment loss depending on the size of the elasticity assumed.[8] Higher wages also affect the sectoral demand for labour (as a factor of production) and other economic variables.

Also critical is the income, or scale effect of broad wage increases.

- On the one hand, a positive income effect refers to the potential for higher wages to raise income and the demand for consumption goods. This is strengthened by the fact that lower-income groups consume more of their wages than is typically spent by higher-income groups. The resulting increase in consumption could lead to higher output, higher labour demand and higher employment.

- On the other hand, rising prices (due to firms’ having higher wage costs) may erode real incomes and lead to falling consumption – a negative scale effect.

Based on reasoning alone, the net impact of higher wages on employment is ambiguous. A particular model’s predictions will depend on how the model’s equations are set out and which of these effects dominate.

Because prices play the dominant role in neo-classical CGE models, ‘the [negative] scale effects dominate’ as noted by both Pauw (2009: 146) and the DPRU (2008: 49). Rising unemployment, in the first instance caused by the substitution of capital for labour on the back a higher labour costs, results in a loss of income. Rising product prices (due to higher wage costs) reduce the buying power of consumer income and thus erode part (or all) of any increase in consumption demand that may be induced by the higher wages. Rising prices also make production inputs more expensive and thus reduce output, and could lead to a potential fall in net exports (depending on assumptions relating to the trade deficit). A predicted depreciation of the domestic currency (in order to maintain the imposed constraint of a constant trade balance) causes higher inflation and real wage erosion, leading to a fall in real income.[9] As a result,aggregate demand is depressed. This leads to further increases in unemployment, with any positive income effect of higher wages more than nullified.[10] This fall in domestic demand and output also results in a fall in firm profits. This chain of events will occur irrespective of the magnitude of the wage-employment elasticity so long as it is negative.

In these models, therefore, gains from higher incomes are always overshadowed by the negative impact of higher labour costs. This occurs by design because the model is constructed in such a way that higher wages will always lead to an initial fall in employment and subsequent fall in income, as well as rising pricing causing additional reductions in income and demand, which will further undermine employment and further reduce demand.

Issue III: Savings and investment in CGE models

Above we noted the importance of assumptions made regarding the direction of causality and the relationship between variables within the equations (such decisions are called ‘closures’). This is particularly important regarding investment and savings, since these variables strongly affect consumption and investment demand in the economy. In these CGE models, the (neoclassical) assumptions automatically augment the predicted contractionary macroeconomic impact of higher wages, as follows.

In a general equilibrium framework, aggregate supply is equal to aggregate demand for all goods and services and all markets clear. This means that, in equilibrium, total investment must be equal to total savings (all expressed as percentages of domestic demand):

![]()

The ‘closure’ selected in these models is to assume that investment as a share of domestic demand (the left-hand side of the equation) is held constant.[11] In addition, it typically is assumed that foreign savings are fixed and that government savings are either fixed or ‘largely unaffected by a minimum wage policy’ (DPRU 2008, p. 84).[12] That leaves only household and firm savings as variable.

The closure that is adopted has two inescapable implications. First, if domestic demand falls when wages are increased (as in the model dynamics described above), the actual level of aggregate investment must also fall in order to keep the left-hand side of the equation (investment as a share of domestic demand) constant. (This can be seen in Table 1, where gross fixed capital formation declines more or less in line with the declining real GDP.)

Secondly, given how the CGE model is constructed, firm profits – and hence firm savings – will fall if prices increase and aggregate demand declines.[13] This means that, in order to keep the equation balanced, the model must predict that household savings will rise: if the left-hand side of the equation is constant, then, as firm savings fall, another type of savings must rise. As Pauw & Leibbrandt (2012, p. 774) note, one sees ‘household savings rates adjusting to ensure equilibrium in the savings market’. Such a rise in household savings necessarily implies a fall in household consumption spending and thus in overall consumption demand, resulting in a further decline in aggregate demand. (This implies a most unusual, and unjustified, assumption that, if wages were to rise, households would not spend them but would rather increase their savings.)

The net effect of the model’s savings-investment assumption is that both investment and consumption necessarily fall when wages increase. This depression of aggregate demand means less output, less investment and lower employment; the economy inescapably deteriorates and unemployment rises when wages increase.

Given how strongly all these assumptions determine the outcome, one would expect the CGE modellers to justify their use. Moreover, they could test the sensitivity of their results to alternative assumptions (such as a Keynesian/structuralist closure in which investment drives savings). Neither the DPRU nor the National Treasury do so. While the likely net impact of using an alternative Keynesian savings and investment closure is theoretically unclear, it is at least possible that rising consumption demand from higher wages may outweigh the negative effects described above.[14] With the neoclassical closure used in the DPRU and National Treasury models this option is precluded by design, so that contraction is the only possible outcome.

Conclusion

We have highlighted two mutually reinforcing biases within the model. The general neoclassical, price-driven architecture of CGE models must result in rising unemployment and economic deterioration in response to higher wages. The unjustified neoclassical assumptions regarding savings and investment further force economic contraction. The models also do not accommodate many real-world adjustments which have been shown to result from implementing minimum wages, and the adjustments that are allowed are those which have been shown to occur very minimally in reality. It is therefore not necessarily the specific characteristics of the South African economy which would cause higher wages to result in unemployment, but the nature of the CGE model and its ad hoc assumptions.

This makes these models unsuitable for modelling the likely impact of a national minimum wage. By construction, in these models the potential positive income impact of higher wages is always overpowered by falling aggregate demand that results in reduced output, declining growth rates and job losses; the possibility of any other outcome is precluded, long before the model predictions are generated.

That these adverse consequences arise even at very low increases in the wage level exemplifies the intrinsic bias of these models. It is difficult to see how the results from these models can be used with good effect to guide policy making with regard to the introduction of a national minimum wage in South Africa.

References

Amlinger M, Bispinck R & Schulten T. 2016. The German Minimum Wage: Experiences and Perspectives after One Year. Institute of Economic and Social Research, WSI-Report 28e.

Arndt C, Davies R & Thurlow J. 2011. The Energy Extension to the South Africa General Equilibrium (SAGE) Model.

Bhorat H & Mayet N. 2013. The impact of sectoral minimum wage laws in South Africa. Econ3x3.

DPRU 2008. Minimum Wages, Employment and Household Poverty: Investigating the Impact of Sectoral Determinations. Development Policy Research Unit.

DPRU 2016. Investigating the feasibility of a national minimum wage for South Africa. University of Cape Town: Development Policy Research Unit.

Gibson B & Van Seventer DE. 2000. Real Wages, Employment and Macroeconomic Policy in a Structuralist Model for South Africa. Journal of African Economies 9(4):512–46.

Isaacs G. 2016. A national minimum wage for South Africa. University of the Witwatersrand, Summary Report No. 1.

Lemos S. 2008. A Survey of the Effects of the Minimum Wage on Prices. Journal of Economic Surveys, 22(1):187–212.

Low Pay Commission 2015. The National Minimum Wage.

MacLeod C. 2015. Measuring the impact of a National Minimum Wage.

Minford P. 1998. Markets Not Stakes. London: Orion Business.

Neumark D & Wascher WL. 2008. Minimum Wages. MIT Press.

Pauw K. 2009. Labour Market Policy and Poverty: Exploring the Macro-Micro Linkages of Minimum Wages and Wage Subsidies. University of Cape Town.

Pauw K & Leibbrandt M. 2012. Minimum Wages and Household Poverty: General Equilibrium Macro–Micro Simulations for South Africa. World Development, 40 (4):771–83.

Schmitt J. 2013. Why Does the Minimum Wage Have No Discernible Effect on Employment?, Centre for Economic and Policy Research.

Schmöller M. 2014. The Introduction of a Minimum Wage in Germany : Background and Potential Employment Effects. Bank of Finland, BoF Online 11.

Stanwix B. 2013. Minimum wages and compliance in South African agriculture. Econ3x3.

Storm S & Isaacs G. 2016. Modelling the impact of a national minimum wage in South Africa: Are general equilibrium models fit for purpose? University of the Witwatersrand, Johannesburg: CSID, Research Brief 1. http://nationalminimumwage.co.za/wp-content/uploads/2016/08/NMW-RI-Research-Brief-1-CGE-Modelling-Final.pdf

Thurlow J. 2004. A Dynamic Computable General Equilibrium (CGE) Model for South Africa: Extending the Static IFPRI Model. Trade and Industrial Policy Strategies (TIPS), Working Paper 1.

Thurlow J & Seventer DEV. 2002. A Standard Computable General Equilibrium Model for South Africa. International Food Policy Research Institute, Trade and Macroeconomics Division Discussion Paper 100.

[1] Both the National Treasury (MacLeod 2015) and the DPRU (2016) use the SAGE model, based on the Standard Computable General Equilibrium Model developed by Löfgren et al. (2002) in the early 2000s for the International Food Policy Research Institute. It was adapted for South Africa by Thurlow & Van Seventer (2002) and further extended in Thurlow (2004) and Arndt et al. (2011). The National Treasury has declined to make their full paper public, so their use of a variant of SAGE is inferred from their October 2015 presentation to Nedlac. The DPRU provides very limited technical information in their published paper and no indication of the model used; however, the DPRU has confirmed, via email, their use of SAGE.

[2] MacLeod (2015) actually gives two sets of output – for the short run and long run. Only the short-run results are presented here due to space limitations and because the assumptions made in the short run correspond with those of the other modelling exercises discussed. The long run results show even greater economic harm from the institution of a national minimum wage (see Storm and Isaacs 2016 for a discussion of both short and long runs). Strictly speaking CGE models do not have a time dimension. The model can be run over a set number of iterations but these do not correspond to an actual number of years in the future. The distinction between short run and long run is on the basis of the assumptions made. That is, the economy is assumed to behave in a certain way in the short run and generate particular results, and then different assumptions are made and this is termed the long run.

[3] These are calculated as weighted averages using slides 16 and 17 of MacLeod (2015).

[4] The wage-employment elasticity is the estimated relationship between changes in wages and changes in employment, for example an elasticity of -0.1 means that a 10% increase in wages results in a 1% fall in employment. The DPRU does not indicate which of the elasticities is considered most appropriate.

[5] See the DPRU (2008); Pauw (2009); Pauw & Leibbrandt (2012).

[6]The DPRU (2008) and Pauw (2009) do exogenously impose productivity increases which reduce job losses.

[7] On unemployment, Schmidtt (2013: 2) notes that the ‘weight of that evidence points to little or no employment response to modest increases in the minimum wage’. All meta-analyses of minimum wage employ effects support this; see Isaacs (2016) for a summary. Regarding rising prices, Neumark & Wascher (2008: 248) summarise that ‘the effect of a minimum wage increase on the overall price level is likely to be small’; Lemos (2008) estimates finds only a 0.4% increase to overall prices from a 10% increase in minimum wages.

[8] Two elasticities are central: the wage-employment elasticity (the ratio of the percentage change in employment to the percentage change in the wage) and the elasticity of substitution between capital and labour (the rate at which different factors of production are substituted for one another, notably how capital use is increased to replace labour as wages rise). The DPRU (2016: 74) notes that ‘employment changes in general equilibrium models depend on the elasticity of substitution and not the wage elasticities, as is the case with partial equilibrium models’. They never give the elasticity of substitution but we assume they derive them from the wage elasticities – and that they are similar in magnitudes – as discussed in the DPRU (2008: 5–6, 87) and Pauw (2009: 39, 251–253). It is unclear how the National Treasury modelling approaches this issue.

[9] In Pauw & Leibbrandt (2012) and the DPRU (2016) the nominal domestic value of the currency depreciates. This is because the trade deficit is assumed fixed and so, when rising domestic prices makes imports more attractive and exports less attractive, the exchange rate depreciates to maintain the trade deficit. A depreciation in the domestic currency leads to higher import costs and higher domestic inflation that erode real wages and household consumption, as well as to higher import costs for firms (which reduce profits). This then causes a decline in domestic demand, firm profits and employment.

[10] Pauw (2009:142) summarises the above: ‘Higher unemployment AND increased prices both erode wage income gains associated with minimum wages, causing disposable income to drop. Reduced levels of disposable income impact negatively on consumption demand, which causes secondary employment and wage income losses due to a decline in labour demand.’ This occurs because of the dominant role of prices in the model. (See in particular equations 50-55, 3-5, 32-38 in Appendix A of Thurlow 2004.)

[11] This is the case for the National Treasury short run but not their long run (see Storm and Isaacs 2016). Also see Thurlow (2004: 9–11) and Pauw & Leibbrandt (2012: 774).

[12] Foreign savings appear not be fixed by the National Treasury but this does not materially alter the analysis.

[13] Savings is a fixed share of capital income (profits). Thurlow notes: ‘Enterprises or firms are the sole recipient of capital income, which they transfer to households after having paid corporate taxes (based on fixed tax rates), saved (based on fixed savings rates), and remitted profits to the rest of the world.’ (2004: 7) Because ‘capital income to enterprises represents gross operating surplus generated during production less activity taxes, and the cost of intermediates and labour remuneration’ (2004: 67) and ‘capital-value-added is gross operating surplus’ (2004: 65), as the quantity of value added, including capital value added, falls due to higher prices and lower demand, so firm profits and firm savings fall.

[14] Gibson & Van Seventer do precisely this in the South African case and find, using a structuralist CGE model, that: ‘if the policy establishment were intent on changing the distribution of income via wage increases, it could do so without loss of employment provided it neutralizes induced policy changes’ (2000: 513).

Download article

Post a commentary

This comment facility is intended for considered commentaries to stimulate substantive debate. Comments may be screened by an editor before they appear online. To comment one must be registered and logged in.

This comment facility is intended for considered commentaries to stimulate substantive debate. Comments may be screened by an editor before they appear online. Please view "Submitting a commentary" for more information.