Soaring deficits and debt: restoring sustainability amidst low economic growth

Introduction

As percentage of GDP the South African government’s debt burden more than doubled since its last low point in 2007, raising fears that fiscal policy in South Africa has become unsustainable. Two questions arise: What does fiscal sustainability entail? And more importantly, is fiscal policy in South Africa unsustainable?

An explanation of fiscal sustainability begins with one of the first things one is taught in economics, namely that human needs are unlimited and resources are scarce. From this follows the lesson learnt early in life: cut your coat according to the cloth. This applies to governments as well – especially because they are custodians of the public purse.

The national budget reflects the sum total of numerous short- and long-term planning decisions made by various government departments and ultimately collated and streamlined by the National Treasury into the budget for the next fiscal year. All of the expenditures by government departments are ultimately financed by taxpayers and the users of government services. If government borrows, the burden is merely shifted to future taxpayers. By inference the financing of government expenditure is fundamentally dependent on the economic resources available in the country.

In the budget, projections of revenue growth from personal and corporate income tax as well as from VAT and the fuel levy are based, to a large extent, on the projections of the growth of total income in the economy (or GDP) in the forthcoming year. Thus, revenue growth depends largely on economic growth. If the projected total revenue is less than the planned total expenditure, there is a projected budget deficit. To enable the government to fund all planned expenditure, it must borrow this amount in financial markets, mainly by selling government bonds to financial institutions and investors. In this way government debt is created – a quite normal occurrence in modern economies.

However, the increase in government debt can get out of hand, increasing fast relative to GDP, thus raising fears about the sustainability of fiscal policy. In this article we clarify the concept of fiscal sustainability and analyse the causes, extent and implications of unsustainable fiscal positions in South Africa. We also propose a way to address the problem. In two follow-up articles we will (1) investigate the role of state-owned enterprises (SOEs) and (2) explore successful ways to regain sound fiscal positions.

The spectre of rising public debt

Public debt is the sum total of the value of all existing government bonds issued plus short-term loans taken out by the government in past years. Or, equivalently, it is the sum of all past annual budget balances (mostly deficits, with surpluses in a few years).

In this article, public debt refers only to national government debt. While most public debt is incurred by the national government, provincial and local governments can also incur debt, if allowed. State-owned enterprises (SOEs) with borrowing powers also accumulate debt, but their debt is usually reported separately from government’s debt. SOEs, together with subnational governments, could be a major potential source of national government debt if they were to default on debt that is explicitly or implicitly guaranteed by the national government. For instance, a very large component of Eskom’s massive debt is guaranteed by the national government.

Assessing fiscal sustainability

Internationally and in South Africa it is not unusual, nor intrinsically remarkable, for the public debt to grow due to recurring annual government budget deficits. This tends to occur particularly during periods of weak economic performance. However, it becomes problematic when, over a number of years, debt increases substantially relative to GDP.

What constitutes ‘substantially’ depends on market and economic conditions such as the appetite of investors to buy government bonds, the trend in the growth rate of GDP and, especially, whether the expected future revenue stream of government is deemed sufficient to cover future debt repayments (in addition to expenditure).

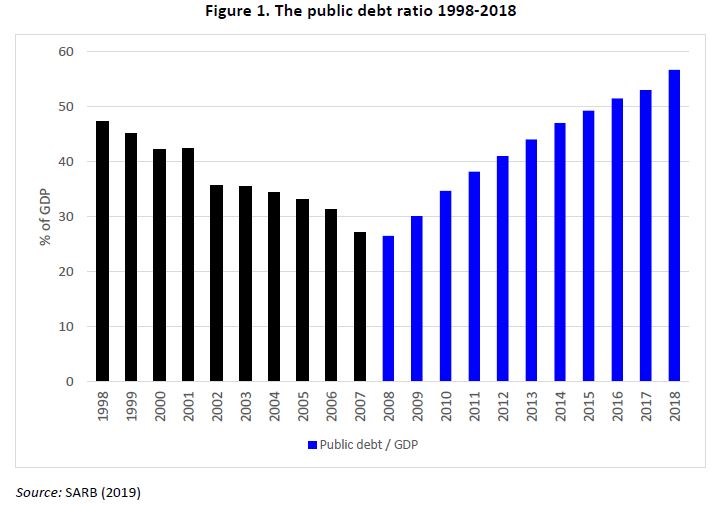

Figure 1 shows that the debt-to-GDP ratio of national government increased from 27.1% at the end of 2007 to 56.7% at the end of 2018. The 2019 Medium-term Budget Policy Statement (National Treasury, 2019: 8) sounded the warning that this ratio may increase to 71.3% at the end of the 2022/23 fiscal year.

There are two approaches to assessing fiscal sustainability. The first defines fiscal sustainability as government solvency, i.e. over time the expected revenue receipts of government are projected to be enough to cover expected expenditure (including interest payments on debt) as well as scheduled debt repayments.[1] Though theoretically clear, this definition is impractical in assessing whether or not fiscal policy is sustainable, as future levels of revenue and expenditure are uncertain or unknown.

In a second, more practical approach, fiscal policy is deemed sustainable if a historical ‘track record’ exists of effective control of government expenditure and tax compliance that can be plausibly projected to be repeated in future, notably in periods when the debt-to-GDP ratio rises markedly. Thus, for instance, should an economic shock or a recession cause the debt-to-GDP ratio to increase, fiscal policy could be deemed sustainable if there were a historical basis for a fair expectation that fiscal control was set to continue in future. This approach to assessing fiscal sustainability thus involves a level of judgement.

Variables that determine fiscal sustainability

A number of key variables determines fiscal sustainability. The first is the ratio between government debt and the country’s gross domestic product (GDP), which is an indicator of the overall ‘size of the economy’. If this debt-to-GDP ratio increased over time, it would signal that public debt was growing faster than the economy was growing. If this continued unabated, the debt would get out of control and fiscal policy would become unsustainable.

The second key variable is the interest payable on public debt. The ability to service the debt depends on the share of tax revenue that must be set aside for interest payments (which must be paid regularly as a legal obligation). As debt increases relative to GDP over time, the interest bill also increases relative to GDP. Any such increases push up the opportunity cost related to the interest cost: every rand spent on interest is a rand not spent on a clinic, or a school, or a hospital.

After reaching its lowest level of 2.3% in fiscal years 2008/09 and 2009/10, the government’s interest bill, as a percentage of GDP, rose to 3.6% in fiscal year 2018/19 – and it is still rising. This may not sound much, until we realise that the interest bill is one and a half times as much as what the agricultural sector produces as a percentage of South African GDP in a whole year, and almost as large as the production of the whole construction industry.

If government is not careful, the fiscal position can deteriorate quickly in the face of rising debt. This is especially likely during protracted periods of low economic growth. This would be true especially if the budget was compiled on the basis of GDP growth forecasts that are too optimistic – something that has plagued South African fiscal forecasts for most of the past decade. Low economic growth means that tax revenues such as income tax, corporate tax and VAT increase at a low rate. The fiscal prospects are worse if, at the same time, government is locked into high expenditure commitments for whatever reason and thus cannot curtail or decrease expenditure. Together these factors can continually push up budget deficits into unhealthy territory.

The interest rate and the primary budget balance

If tax revenue exceeds the government’s non-interest expenditure (i.e. expenditure on defence, housing, education, health, etc.), it means that government has some tax revenue left over to pay (some of) the interest. This means there is a so-called primary budget surplus. (The primary budget balance plus the interest bill comprises the conventional or overall budget balance. For more detail, see Fourie & Burger (2019), Chapter 10.7.)

If tax revenue is not even enough to pay for the non-interest expenditure – i.e. when there is a primary budget deficit – government will have to borrow to pay all the interest (and more). Thus, the total amount of the annual interest will be added to the debt. The higher the interest rate on debt, the larger this addition to the debt will be.

Together with the size of the primary deficit, the risk of fiscal unsustainability depends crucially on the interplay between (a) the real interest rate on government debt and (b) the real GDP growth rate.

If there is a primary deficit while the real interest rate on government debt is higher than the real GDP growth rate, the public debt will increase faster than GDP. To prevent this from happening, the government should rather be running a sufficiently large primary surplus,[2] i.e. its non-interest expenditure should be less than the tax revenue. To achieve that, the government should either cut back its non-interest expenditure or increase its tax revenue.

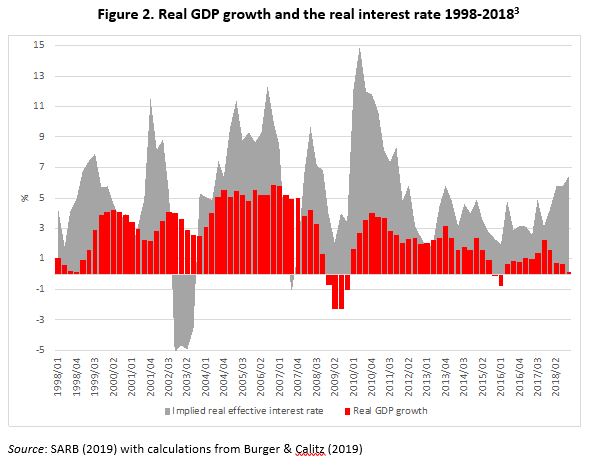

A general rule of thumb is that, to a limited extent, a primary deficit can be maintained without an increase in the government’s debt-to-GDP ratio, provided the real rate of economic growth is higher than the real rate of interest on government debt. Such a situation exists in the US and some other OECD countries, but not South Africa. Figure 2 shows how persistently the economic growth rate (the red bars) has been below the real interest rate in South Africa in the past two decades.

This means that most of the time South Africa could not afford, fiscally, to have had a primary budget deficit at all. It needed and still needs primary surpluses – and ones that are relatively large.

The primary budget balance in practice: is fiscal sustainability a priority?

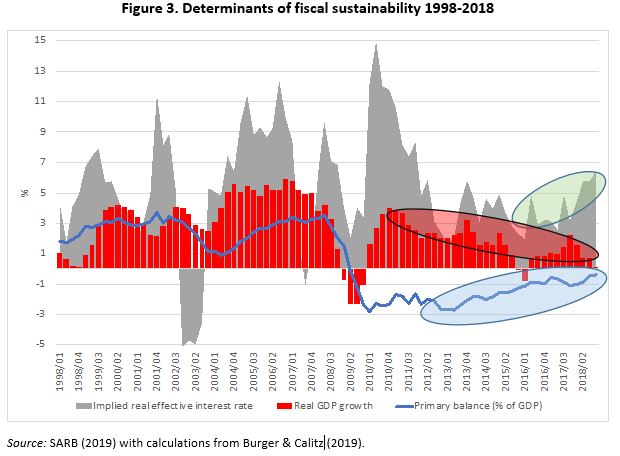

We analysed the impact of the increase in public debt in South Africa in a recent paper (Burger & Calitz 2019: 10-11). The objective was to deduce the extent to which government has prioritised fiscal sustainability by running sufficiently large primary budget surpluses.

Figure 3 below combines figure 2 with data on the primary budget balance to show the overall fiscal sustainability position:

- The rising debt-to-GDP debt ratio from 2008 to 2019 (as in figure 1) coincided with a declining economic growth rate (from 2011 to 2018 – red oval in figure 3) and a rising real interest rate (from 2015 to 2018 – green oval in figure 3).

- Although the primary balance (as a percentage of GDP) improved (blue oval in figure 3), it was not nearly sufficient to offset the rising debt-to-GDP ratio – in fact, it remained in deficit territory, never registering the surplus needed to stabilise the debt-to-GDP ratio.

Thus, although the government appears to have taken steps since 2008 to arrest the increase in the debt-to-GDP ratio, those steps were just not enough. Clearly, fiscal sustainability was not at the top of government’s fiscal priority list.

Next we look at the behaviour of the components that constitute the primary balance. We find the following:

- In response to the increasing public debt-to-GDP ratio during the period 1996 to 2018, the total-revenue-to-GDP ratio increased, but only marginally.

- However, since 2009 the total non-interest expenditure-to-GDP ratio did not respond to changes in the debt-to-GDP ratio.

Thus, the ‘recovery’ observed in the primary-balance-to-GDP ratio during the last decade was due to the ‘performance’ of the revenue-to-GDP ratio and not to ratio of non-interest expenditure to GDP. Expenditure was not sufficiently curtailed.

In short: though revenue failed to stabilise the debt-to-GDP ratio, it helped to prevent the debt-to-GDP ratio from increasing even faster. However, the expenditure side of the budget did not help in this regard at all, leaving the debt ratio growing persistently.

What primary budget balance is necessary to stabilise the debt-to-GDP ratio?

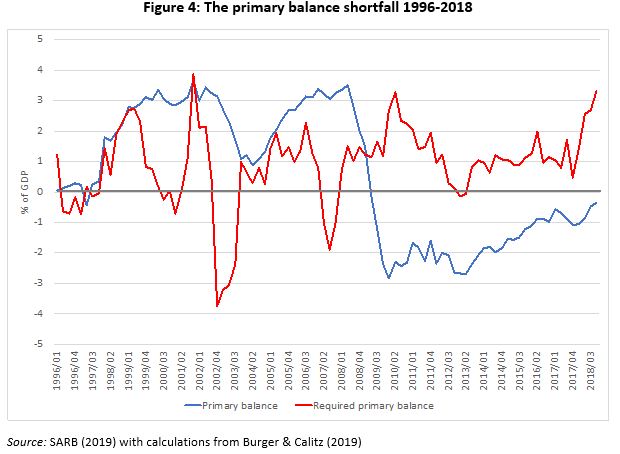

It is interesting to analyse how much the primary balance fell short of what was required to stabilise the debt-to-GDP ratio after 2008/09. Figure 4 contrasts the actual primary-balance-to-GDP ratio (blue line) in each year since 1996 with the primary-balance-to-GDP ratio that would have stabilised the debt-to-GDP ratio at its level in the previous year (red line).[3]

From 1999 to 2008 the actual primary-balance-to-GDP ratio exceeded the required primary-balance-to-GDP ratio, which explains why the debt-to-GDP ratio fell during this period (see figure 1). However, the reverse holds for the period since 2009 – with ominous consequences for the debt-to-GDP ratio.

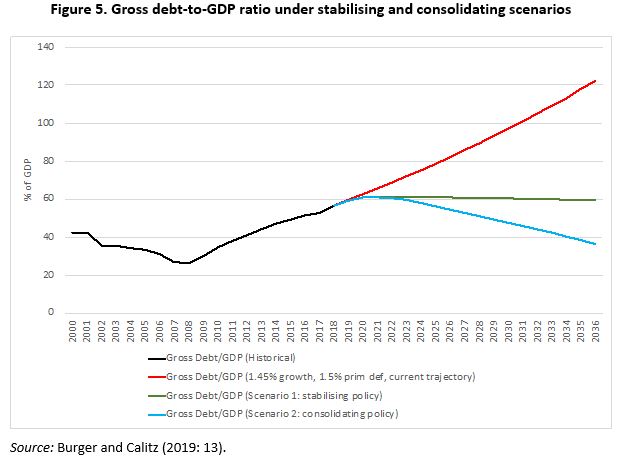

What will it take, by way of changes in the primary balance, to restore fiscal sustainability? In figure 5 we present three possible future fiscal paths, indicative of the wide range of possible outcomes.

The top (red) line in the diagram projects the debt-to-GDP ratio if the present trend continues: it will breach 100% around 2030. The other two lines portray developments on the assumption that the economic growth rate slowly improves to a modest 2.5% by 2023. Two forms of fiscal policy are simulated:

(a) In the case of a stabilising policy strategy to ensure that debt-to-GDP increases no further, the primary balance needs to improve from a deficit of 1% of GDP in 2019 to a surplus of 1% by 2021 (scenario 1, green line). This means that by 2021, compared to 2019, either government expenditure will need to undergo reductions equivalent to two percentage points of GDP, or taxes must generate such extra revenue – or some combination of the two.

(b) In the case of a consolidating fiscal strategy (scenario 2, blue line) which aims to reduce debt-to-GDP to below 50% by 2030, the primary balance needs to improve from a primary deficit of 1% of GDP in 2019 to a primary surplus of 2.5% of GDP by 2023. (Targeting the later date in this case, i.e. 2023 instead of 2021, is more realistic because the required fiscal reform is more severe and may take time to implement.) With reference to our earlier explanation of fiscal sustainability, the fiscal track record in the past decade is not a good predictor that this primary surplus could be achieved, unless decisive and plausible measures are taken.

Both scenarios will therefore require very stringent fiscal policy measures. Especially a reduction in debt-to-GDP (scenario 2) will require quite drastic measures, unless the economy performs much better. Notably, it will require economic growth exceeding 2.5% per year, returning to the levels of 3% to 5.5% last seen from 2003 to 2008.

The type of fiscal consolidation policies likely to be considered and the implications of the debt of state-owned enterprises for fiscal reform, will form the subject of two forthcoming articles on Econ3x3.

Is there a case for fiscal stimulus? To the contrary ...

Recently voices were raised to argue that, instead of fiscal consolidation, South Africa needs more fiscal stimulus in the form of larger, not smaller budget deficits. The rationale is that by spending more, the government would stimulate economic growth, causing the denominator in the debt-to-GDP ratio to grow faster than the numerator.

This is unlikely to succeed. As shown above, an improvement in the primary balance from ‑1% of GDP to 1% of GDP, together with an improvement in the economic growth rate to 2.5% by 2023, would be just enough to stabilise the ratio. If the primary deficit had to become larger (instead of shrinking and becoming a surplus) in pursuit of a 2.5% economic growth rate, the debt-to-GDP ratio would clearly not stabilise (not to mention decrease). South Africa simply cannot spend its way out of a high and increasing debt burden.

It is to be noted that the large fiscal deficits of the last decade all failed to stimulate growth. There is little, if any, evidence that a debt-financed stimulating fiscal policy will be growth-enhancing (let alone to the extent needed to prevent further increases in the debt-to-GDP ratio).

Increasing government spending to stimulate the economy also confuses cyclical with structural policy. South Africa’s current low economic growth rate is the product of a low structural growth trend, not of an economy underperforming cyclically relative to a higher growth trend. Cyclical fiscal stimulation is therefore unlikely to restore higher economic growth structurally. What the South African economy needs is coherent structural reforms that will unleash investment that will expand the productive capacity of the economy.

Having said this, we are not proposing a sharp fiscal contraction to reduce the debt-to-GDP ratio in the next five years. Such a policy would probably cause a severe contraction in an economy that already suffers from extreme levels of unemployment and would also be politically difficulty to implement.

What we propose is the following:

1. Until such time as economic growth picks up to levels of 2% or more, the government should focus on merely stabilising the debt-to-GDP ratio. Once economic growth reaches 2%, the focus can shift to reducing the debt-to-GDP ratio.

2. The stabilisation of the debt-to-GDP ratio should be phased in over the medium term. Stabilisation requires attaining an aggregate reduction in the budget deficit of between 2% and 3% of GDP, but it should be done over a three- to four-year period.[4] Most of this adjustment needs to come from reducing government expenditure, as there is little room to increase taxes if investment is not to be discouraged any further. (The size of the reduction will depend on whether or not growth improves: if growth gets up to 2.5%, the required expenditure reduction will be closer to 2% of GDP.)

Conclusion

Reaching a cut in the level of government expenditure of 2% to 3% of GDP – approximately R100 to R150 billion in 2020 rand terms – by 2023/24 is significant, but it is necessary to stabilise the debt-to-GDP ratio and for government to regain some fiscal credibility. It represents the first steps on the road back to fiscal sustainability. Reducing the debt-to-GDP ratio could then be achieved later by relying on higher economic growth, right-sizing the civil service and terminating support to financially unsustainable (i.e. bankrupt) SOEs. Failing to make the cut in expenditure will only postpone the inevitable and enlarge the expenditure cut that will ultimately have to be made.

References

Burger P & Calitz E. 2019. Sustainable fiscal policy and economic growth in South Africa. Stellenbosch Working Paper Series No. WP15/2019.

Fourie FCvN & Burger P. 2019. How to think and reason in Macroeconomics – A South African Text, 5th edition. Juta, Cape Town.

IMF (International Monetary Fund) 2020. South Africa: 2019 Article IV Consultation-Press Release; and Staff Report; and Statement by the Executive Director for South Africa. IMF, Washington DC.

National Treasury 2019. Medium-term Budget Policy Statement. Pretoria.

[1] More formally: if the present value of the expected flow of all future revenues exceeds the value of outstanding debt plus the present value of all future government expenditure.

[2] If it is not large enough, the debt/GDP ratio will keep on increasing.

[3] The debt-to-GDP ratio which we use to calculate the required primary balance is therefore a moving target; each year it is reset at the level of the actual debt-to-GDP ratio of the previous year.

[4] This proposal is more moderate than the IMF’s proposal, in its January 2020 Article IV Statement, of a gradual expenditure cut of 4%-4.5% of GDP. The IMF’s proposal also factors in additional assistance to SOEs that will further increase the debt-to-GDP ratio. Should economic growth not recover at all, a cut closer to the IMF’s proposal becomes warranted.

Download article

Post a commentary

This comment facility is intended for considered commentaries to stimulate substantive debate. Comments may be screened by an editor before they appear online. To comment one must be registered and logged in.

This comment facility is intended for considered commentaries to stimulate substantive debate. Comments may be screened by an editor before they appear online. Please view "Submitting a commentary" for more information.